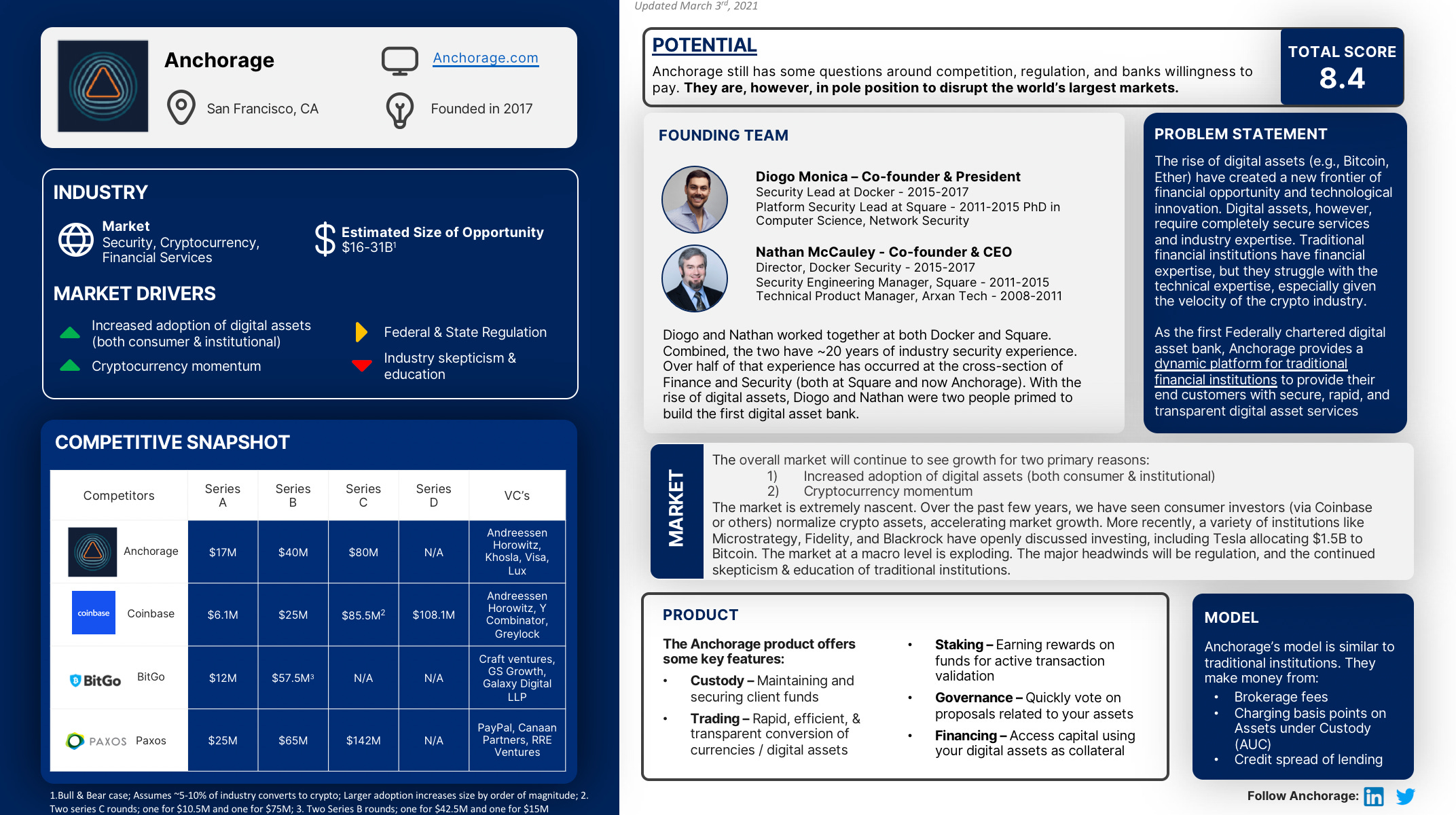

Every day, founders & operators everywhere are building new technologies and companies that should us optimistic about tomorrow. My goal: champion some of these founders, companies, and industry trends. Join thousands of investors, operators, and founders on the mailing list!!

The Bank of the Future

On January 13th, Anchorage received the first federal bank charter in US history from the Office of the Comptroller of the Currency (OCC). The adoption of cryptocurrency has been a point of debate for years, but with this move, the Federal government gave the largest stamp of approval to date.

Tesla broke the barrier by purchasing $1.5B in Bitcoin. It will soon be commonplace for large institutions to begin holding and leveraging digital assets. Crypto, however, can be a technical challenge for traditional institutions. The velocity of the space can be a challenge. Blockchain technology is fairly nascent, and it is not a traditional skillset.

This is where Anchorage comes in.

With Anchorage’s digital asset platform, traditional financial institutions can instantly access the most sophisticated, transparent cryptocurrency financial services to date. In Diogo Monica (President) & Nathan McCauley’s (CEO) announcement post, they clearly state that Anchorage has “been credited numerous times with blurring the lines between crypto and traditional finance. Today, we’re happy to see those lines begin to be erased.”

The bank of the 21st century has finally arrived.

Summary

Exhibit 1: The Five Anchorage Products

Currently, Anchorage offers five key products (Exhibit 1) to optimize the value of digital assets:

Custody – Maintaining and securing client funds

Trading – Rapid, efficient, and transparent conversion of currencies / digital assets

Staking – Earning rewards on funds for active transaction validation

Governance – Quickly vote on proposals related to your assets

Financing – Access capital using your digital assets as collateral

Each of the products is pretty typical for traditional financial institutions. Digital assets are not. The Bank of New York Mellon was founded by Alexander Hamilton. With over 200 years of history, even they are entering a new space, announcing their adoption of Bitcoin.

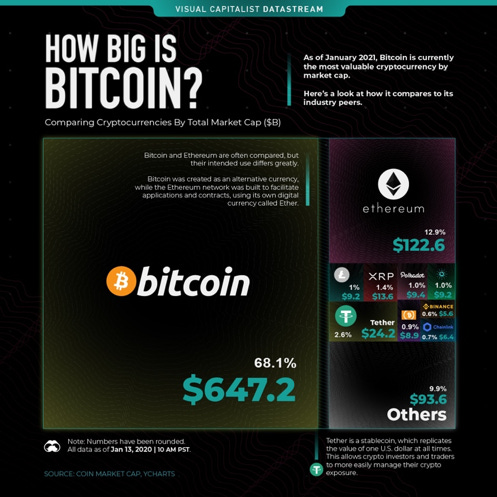

On October 31st, 2008, finance unknowingly encountered the scariest Halloween Ghoul they could imagine: Bitcoin. Since Satoshi Nakamoto published the original whitepaper, Bitcoin has gone from a market cap of $0 to $1 Trillion. Along the way, numerous additional assets have been created (e.g., Ethereum, Litecoin). The space has exploded.

Exhibit 2: Market cap of cryptocurrencies (as of 1/13/20) Source

Similar to traditional car companies trying to compete with Tesla, banks are likely already struggling with the concept of building entire blockchain-focused, cutting edge crypto services. Anchorage, however, steps in and provides the digital asset platform that can bring banks from digitally nascent to digitally native in a day. Basically, if you are a bank and you qualify to provide digital assets to your consumers, then Anchorage can help you do that securely, quickly, and transparently.

The economics of purchasing the platform versus building makes sense. Anchorage has the first mover advantage, as well as the expertise. Both Diogo Monica and Nathan McCauley (the founders), helped build initial security infrastructure at Square, as well as Docker. The two founders have 10+ years of network security, most of it coming at the cross-section of financial infrastructure. In their OCC charter announcement, McCauley and Monica highlight both their first mover advantage, as well as the need for agility:

“Before now, there have existed fintech companies with the technical sophistication to securely handle digital assets under a piecemeal, state-by-state regulatory structure, and there have existed federally chartered banks with a robust regulatory framework that lack the true technological savvy it takes to operate in the blockchain space at its breakneck pace of innovation. Anchorage Digital Bank is the first entity to have both the tech and the regulatory clarity that serious institutional participation in crypto demands.”

Overnight, Anchorage is bringing banks from digital nascent to digital native.

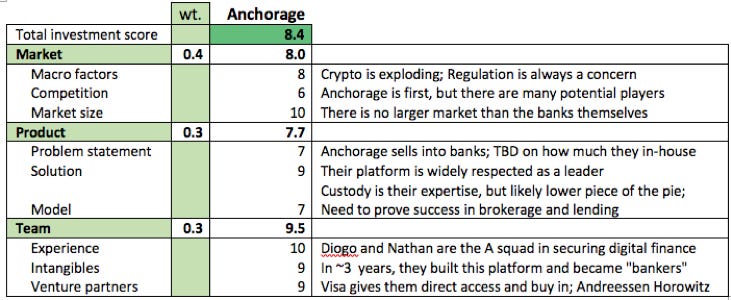

Investment score

Exhibit 3: Anchorage investment score overview

Anchorage is in a massive market being disrupted, and they have the perfect team to do it. The three questions that will determine a lot of value:

What will US policy on crypto be moving forward?

Will indirect competitors (e.g., Coinbase, Square) migrate into banking?

How much of the financial sector will be shift to digital assets?

Question #1 & #3, in particular, could increase or decrease the TAM by an order of magnitude.

Conclusion

Anchorage checks all of the boxes. First to market. Technical expertise. Strong venture backing and partners. Exploding market. Overall, there are many competitive players, but the space is large enough for 2-3 players to capture significant share. As long as crypto adoption continues, Anchorage is a rocket ship that is never returning to earth.

Appendix: Battlecard Backups

Problem Statement

Crypto continues to grow exponentially. Now, traditional funds (e.g., pensions, retirements, corporate) are beginning to adopt. Traditional institutions do not have the technical expertise, resources, or agility to build a new digital platform rapidly and at scale.

What is the market opportunity?

Very few people can agree on the end state size of cryptocurrency. To simplify, let’s just look at some fundamental drivers for Anchorage.

Growth drivers:

Increased Adoption of Digital Assets – Regardless of skeptics, it is clear: people are adopting. Bitcoin’s market cap broke $1T. In 2019, Coinbase passed Schwab in number of users. In addition, companies like Paypal, CashApp, Wayfair, Tesla, etc. are increasingly coming forward stating they are open to receive crypto as a form of payment

Cryptocurrency momentum – Beyond just adoption, the momentum is critical. Crypto has significant network effects. As adoption increases, it becomes increasingly useful at a transaction level. The current momentum and rapid adoption is critical to reaching the tipping point.

Uncertain factors

Federal & State Regulation – One of the biggest concerns for cryptocurrency is regulation. The recent approval of Anchorage for a Federal charter is a strong sign of support. Globally, there are signs government institutions are open to the idea. This all, however, can change with new administrations. For crypto, the genie is likely out of the bottle, but regulation will always be the immediate uncertainty

Challenges:

Industry skepticism & education – Traditional investors have remained wary of crypto. The large increases in value have converted many, but until large, passive money floods in, it will be difficult to see a world where volatility decreases. High volatility will always be enough to scare institutions out of crypto. I view this challenge as very low, but it will continue to be an ongoing effort.

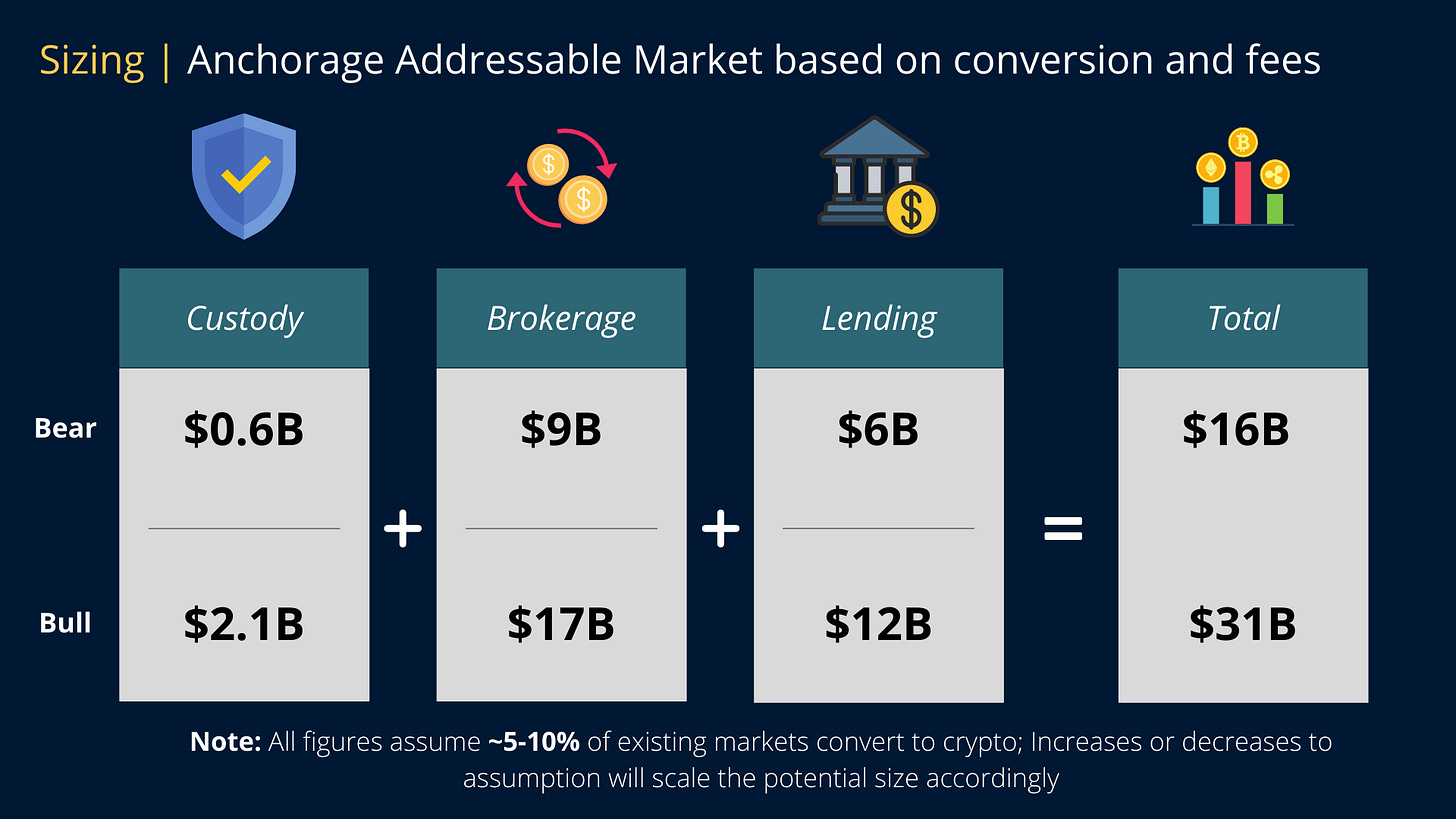

How big is the market?

Anchorage’s business model makes money three ways:

Assets Under Custody,

Brokerage Fees

Spread on Loan Origination.

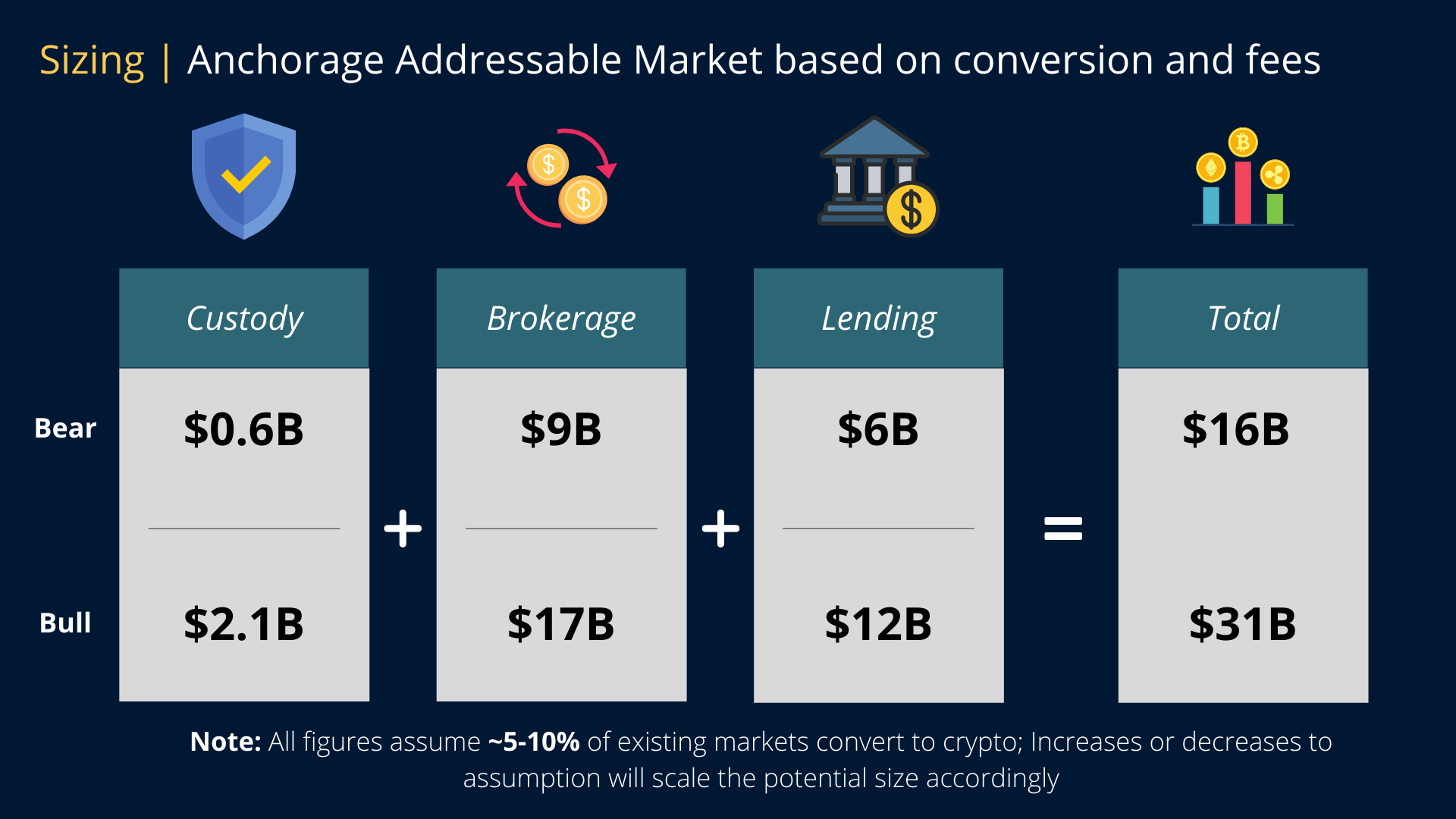

Exhibit 4: Anchorage opportunity sizing

Looking at moderate assumptions of adoption, fees, and market sizes, the TAM for Anchorage is ~$11-21B. A few high-level insights:

Custody drives <10% of the overall business, but strategically, actively securing crypto is a huge value add, as well as a requirement for lending

Unlike many $0 fee equity trading apps, the industry standard, Coinbase, charges are fairly sizable fee. Even by drastically undercutting Coinbase, there is sizable opportunity in brokerage

The largest value (+50%) comes from Anchorage’s ability to lend

A few disclaimers:

These estimates are for US only

In every assumption or sizing, I chose to operate conservatively

As a result, higher crypto adoption, global coverage by US digital banks, and higher end fees could raise these estimates by an order of magnitude

Step-by-step market sizing

Assets Under Custody

$21.22T in total assets within banks per the FDIC (3Q 2020)

JP Morgan charges from 0.30-1.45% in custodial fees (Source: SmartAsset)

Assumed (long-term) ~5-10% of total assets are digital

Assume digital platform charges 5-10 basis points

~$0.6-2.1B in TAM for US assets under custody

Brokerage Fees

Option A:

US brokerage market ~$343B in 2020 growing at CAGR of 3.4%(Source: KenResearch)

Assumed (long-term) ~5-10% of total brokerage volume on crypto

Assumed digital platform has ~50% take rate

~$9-17B in TAM for crypto brokerage fees

Option B:

$1.82T in crypto trading volume in 2020

Binance charges 7-10 bps

Coinbase charges 1.49% of volume

Assume lower end of 7-10bps

~$1.2-$1.8B

Spread on Loan Origination

$10.9T in total loans per the FDIC (3Q 2020)

~5-10% of lending long-term converts to crypto

Anchorage both originates loans and facilitates for customers (e.g., Silvergate)

Assume 100% of loan activity is direct; Bank of America 2019 net interest margin of 1.14%, BNY 2019 net interest margin of 1.10%; 2018 BNY net interest margin of 1.25%; Assume ~1.10%

~$6.0-12.0B in TAM for facilitating loans in US

Competition

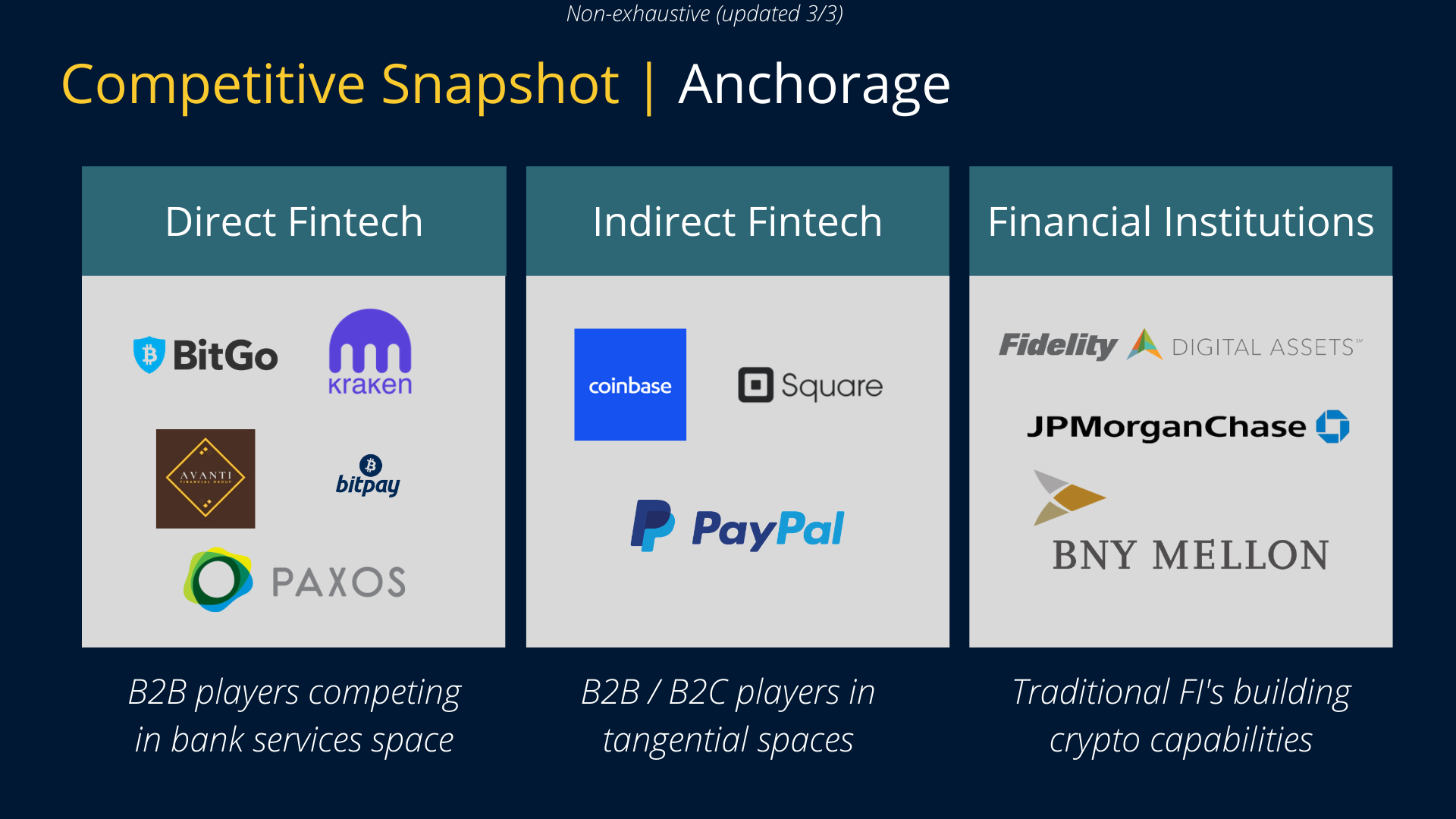

Exhibit 5: Anchorage competitive snapshot

There are quite a few institutions competing with Anchorage. The competition includes three groups in my mind:

Direct fintech companies – B2B players offering direct, competitive offerings

Indirect fintech companies – B2C / B2B players focused on tangential offerings; Could be competition or partners long-term

Institutional players – Traditional finance building technical offerings; Could be built in-house (competition) or purchased (potential customer)

Direct Fintech Competitors

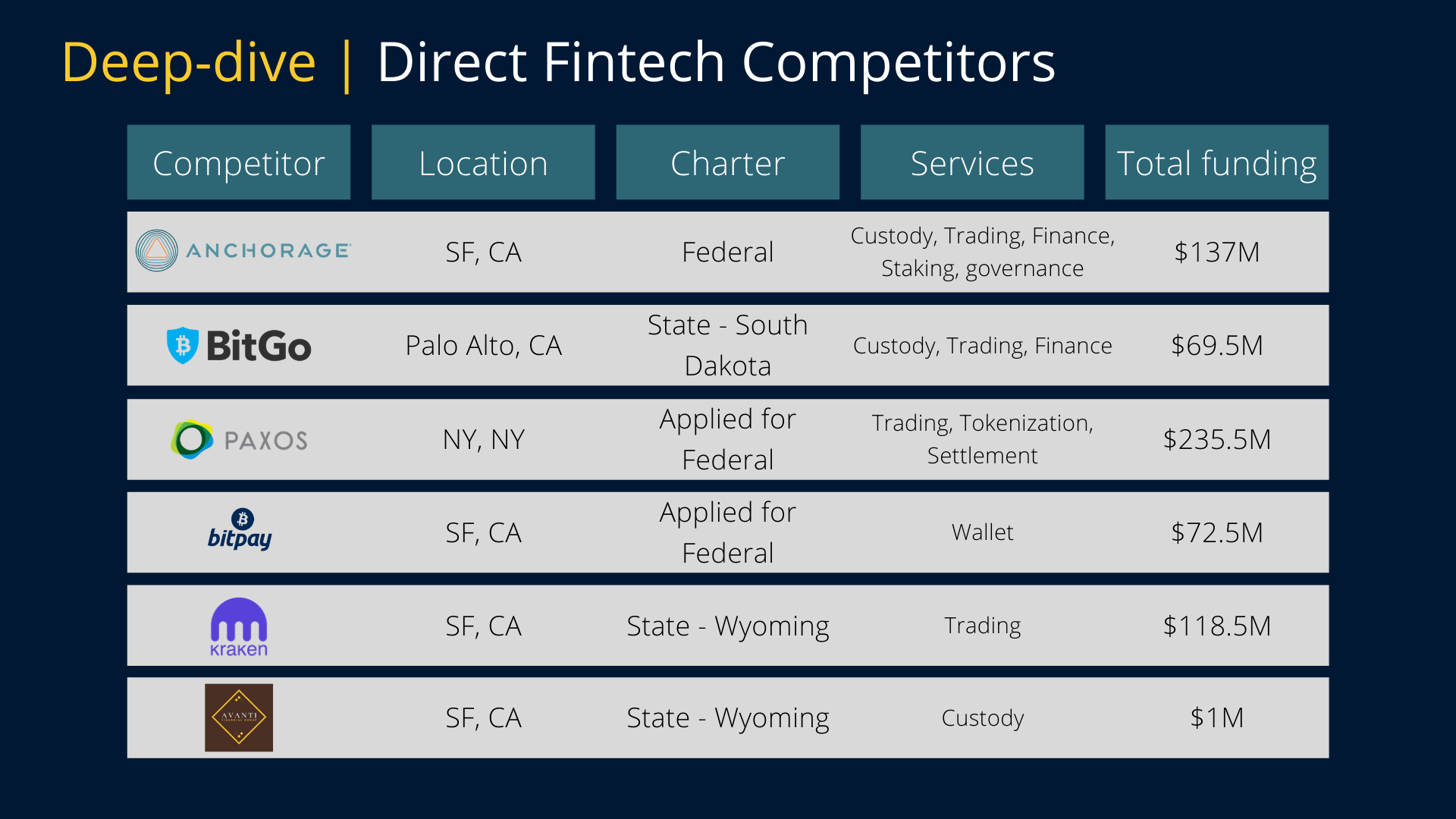

Exhibit 6: Deep-dive of Fintech competitors

Within the direct Fintech space, I have highlighted five companies:

BitGo – Seems to be most direct competitor; Limited by state charter

Paxos – Most formidable competitor; Significant Series C funding; Applied for Federal charter; Focused on provided a digital asset bank platform; Less emphasis on staking, governance, and financing at this moment

Bitpay – Secure wallet; Partnered with Mastercard (Anchorage is partnered with Visa); Application for federal charter would allow for expansion into competitive spaces with Anchorage

Kraken – primarily focused on brokerage;Significant funding and state bank charter make expansion to alternative financial services possible

Avanti – Limited information and funding; Seems to be most focused on forming a true digital bank, mirroring traditional financial institutions

Indirect Fintech Competitors

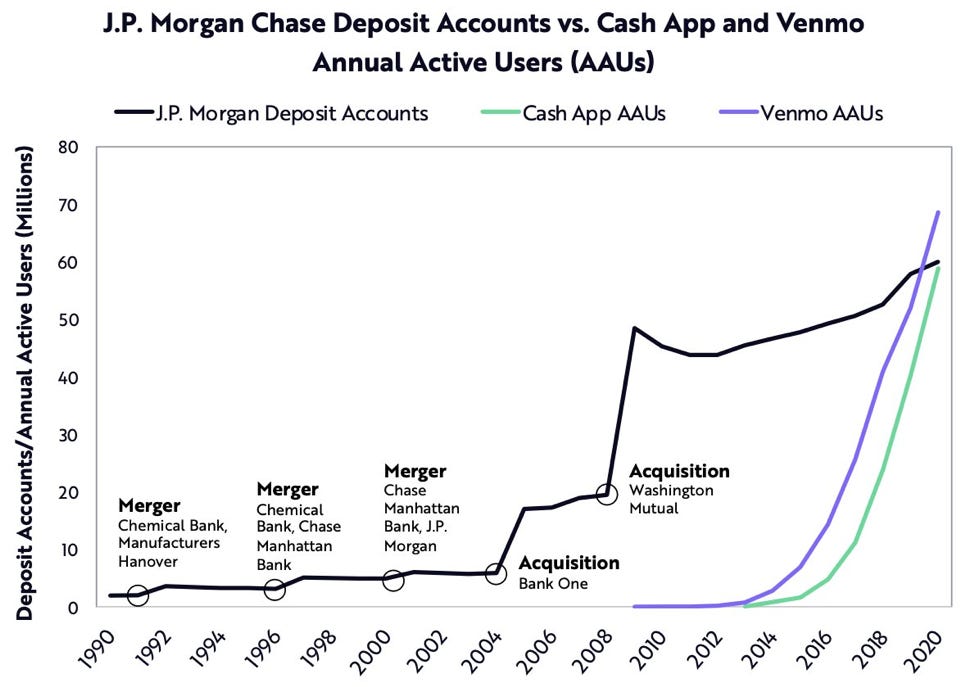

Square – Mammoth of the industry; Largest size and reach, particularly within SMB; CashApp Annual Active Users exceeded 70M in 2020 (Exhibit 5); Recently announced Federal bank charter; TBD on whether they will offer crypto specific services; I think Anchorage could be a great acquisition for Square a few years from now

Coinbase – Well-backed (both financially and with industry players); Strong control of retail market; B2C; Could use strong consumer hold to migrate up-market

Paypal – Second largest player payments player; Venmo Annual Active Users ~60M in 2020

The three main players in this space pose an interesting potential partner and competitor dynamic. All three provide retail investors with access to crypto, but as shown recently, Coinbase helped Tesla acquire large scale of Bitcoin. Likely, I think these three stick to their core business, and they partner with a chartered bank like Anchorage to execute traditional financial institutions, but there is a world where one of these companies migrates up the chain and competes directly with Anchorage. I see this as the biggest threat.

Institutional Competitors:

Fidelity Digital Assets

JPMorgan Chase

Bank of New York Mellon

Deustche Bank

There is still slightly limited information on the capabilities of each institution. Fidelity Digital Assets appears to be the most advanced with $13B in digital AUM. For the others, the conversation has just begun. Oddly, the most mature businesses are the most nascent in their digital strategy. For this very reason, many are likely to turn directly to the Anchorage’s of the world and become customers. I think there is limited threat of true competition here.

Exhibit 7: Average Annual Users for JP Morgan, CashApp, and Venmo; Source

The list is non-exhaustive, but I have listed them in order of both size and level of competition (from my perspective).

Please check https://chudovo.de/the-requirements-to-build-an-ecommerce-website/