Sutter Hill Ventures: The Silent Builders of Silicon Valley

A breakdown on Sutter Hill Ventures Origination Playbook

One of the oldest, most successful firms in Silicon Valley is likely one you have sparingly heard about: Sutter Hill Ventures (SHV).

This is by design. SHV purposefully keeps a very low profile, and they do things VERY differently than most firms. But silently, SHV has been building large companies for years.

But these are VCs! Why am I giving them so much credit for building? That's where it gets interesting. SHV "originates" companies. This means they build companies from scratch, from day one to IPO. From Crunchbase & LinkedIn, I was able to identify 20 companies they have helped found since 2009:

Almost $100B in market cap created, and that is going to grow RAPIDLY. Most of the value is anchored in Snowflake, but Sigma Computing & Lacework are showing early signs of being the next great ones. And it appears the rate of origination is increasing.

The big pivot to origination began in 2008 when Mike Speiser joined SHV. They began the practice by creating Pure Storage. Since then, it appears the firm has increasingly shifted their weight to originating companies. Since 2009, I identified ~80 different SHV portfolio companies. 20 of those counted SHV as founding investors, and 10+ had SHV in-residence builders as founders.

Big disclaimer: I have never seen the inside of Sutter Hill Ventures, and I have not spoken to anyone at SHV about their strategy. Speiser does not do media, so it is likely that we will never know, but in my writing about Sigma Computing (a Sutter Hill Ventures origination), I read a lot about the firm.

I am fascinated, so I did my best to distill ten of their operating principles:

While some of these seem more important than others, they all tie together. Without a single component, the model may not work. So let's walk through it.

Philosophy: Stay focused & build big sh*t

Three principles: 1) Build it, 2) Fewer bets, more focus, and 3) Big bets.

1) Build it

The first major distinction between SHV and other VCs is that SHV builds.

At SHV, they refer to it as 'originating' a company. Elsewhere, you may hear it referred to as 'incubating' companies.

This is not an Erlich Bachman and Jian Yang (from Silicon Valley) scenario where SHV just gives office space & resources to companies for a cut of the pie. No. They actually get into the weeds on a day-to-day basis and plan on building (more on 'how' in the process section).

Their track record shows they are serious about it. Of the ~80 companies they invested in, they helped found 20 of them. ~25% of their portfolio is focused on actually building.

2) Fewer bets, more focus

Venture Capital, however, is an industry that tends to rely on velocity (how quickly you deploy) and diversification (how many different companies you can back). Startups are very uncertain. If you invest in two and one fails, then you are in trouble. If you invest in ten and one fails, then you can make up for it!

2021 was a particularly chaotic year, but if you look at the capital deployed by the top 10, every one of these firms made 50+ deals. Tiger, Softbank, and Coatue are all traditional mega-funds jumping into VC, so their velocity of 100+ deals may not be surprising.

But Andreessen Horowitz (AH Capital Management LLC) and Sequoia Capital are two of the top VC firms (in both name & performance). They both surpassed 100+ deals.

According to Crunchbase, SHV only did seven deals in 2021. Total capital (including other firm contributions) was ~$3.1B for these seven deals, so they were... huge (Lacework alone was $1.3B).

SHV will only originate ~1-2 companies per year, and then they selectively pick a few other investments. Originating & build companies is difficult, so SHV makes much fewer bets, and remains laser focused on their priorities & current investments.

3) Think big

Being this hyper-focused means there is a potential MASSIVE opportunity cost. SHV has to say no to opportunities, and they better be sure the 1-2 they choose are winners.

For this reason, all of their companies are 'big bets.' What do I mean by this?

Large macro trends (e.g., shift to cloud storage)

Long-term problems (e.g., leveraging cloud data)

Difficult technical solve

Massive market (e.g., >1B ARR potential)

First, SHV identifies large macroeconomic shifts. Trends that are here to stay. Examples include the shift to cloud (ex. Snowflake) and flash storage (ex. Pure Storage). These trends are the rising tide that will lift all ships. SHV is particularly good at seeing these early.

Once they have identified one of these trends, the question becomes: what is a current (or soon to be) problem that we can go solve? Then they solve it.

More often than not, these are hairy, challenging problems. But in a way, that's by design. These are not quick, off-the-shelf solves that can be replicated. These are unique solutions, and when they get it, it is special.

If they are going to put in the effort to solve this problem, then the market has to be huge. The payout has to be there. The goal is to scale to +$1B in annual revenue.

I wrote about a recent example: Sigma Computing. Here is how it compares to this framework:

Large macro trend → Growth of cloud data infrastructure

Long-term problem → SQL bottlenecks D&A teams & prevents business leaders from leverage cloud data tools

Difficult technical solve → Providing spreadsheet functionality on the cloud data warehouse

Massive market → Business Intelligence tools

Process: Find experts, stay agile, and then go...FAST

Four principles: 4) Recruit the experts, 5) 40% model, 6) stay agile early, and 7) go fast.

4) Recruit the experts

So, the question is... how do they do this? The first step: bring in the experts.

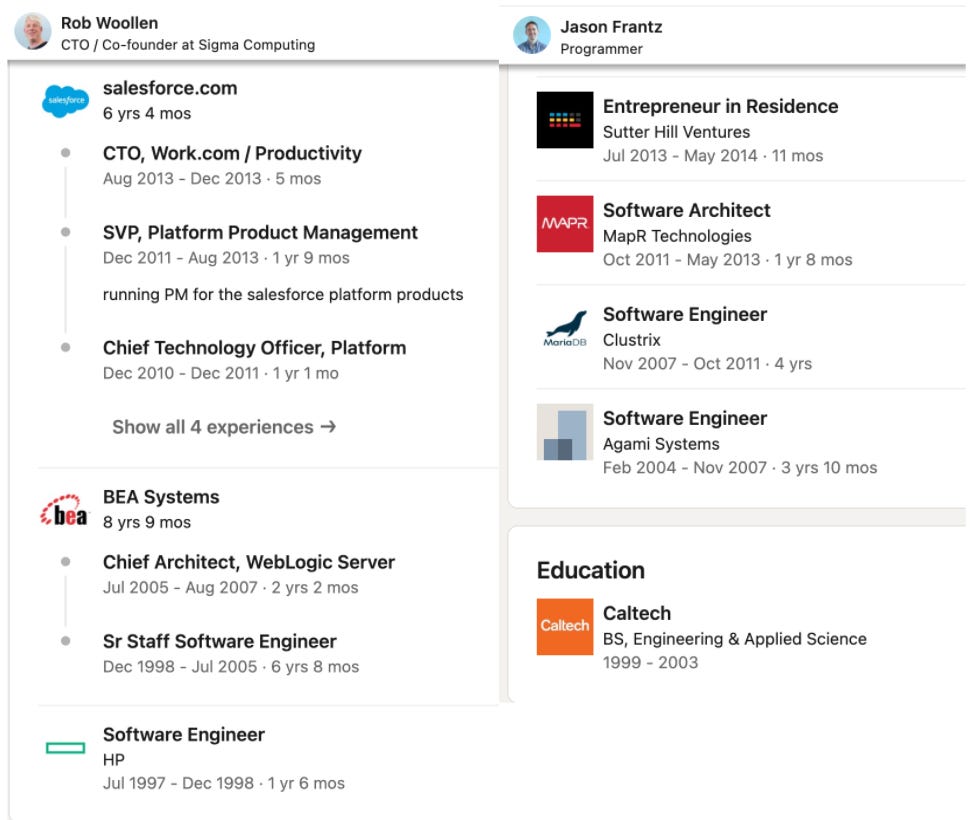

If you look at the founders of SHV companies, they are incredibly well-established & experienced people.

In other words, SHV has a deep network within technical fields. When they want to originate companies, they do not go to college campuses. They find people who have been working in these large B2B fields for years, and they source the best-of-the-best.

5) The 40% model

You may notice that the founding teams are entirely technical. Feels like a skillset gap on the business & operations side. This is by design.

When the companies are originated, Speiser operates on the 40% model. Two days of the week are solely focused on the company being originated. The other three days he focuses on supporting all other portfolio companies.

By stepping in for two days a week, Speiser essentially handles most of the operations and dirty work (e.g., recruiting, sales, finance). My hypothesis is that the entire SHV staff leans in to help portfolio companies with different areas (more in "Hire Operators").

This allows the founders (aka the experts) to focus solely on building a new product. No worries about recruiting, fundraising, burn rate, etc. Their entire focus is on solving the identified problem.

And it should be noted... Speiser has done this many times, so he is EXTREMELY good at it. This is an incredible flywheel. Most people hate the dirty work in the beginning. He takes it on continuously. And recruiting & building early teams is one of his biggest strengths.

In the story about building Pure Storage, Speiser is mentioned 13 times. Other than table of contents mentions, every Speiser mention was based on him recruiting for the founding team. He has an immense network. He finds good builders. He assembles amazing teams.

Note: this is not just exclusive to Speiser; Doug Mohr, SHV Managing Director, is mentioned many times in the same capacity.

6) Stay agile early

In this early stage, SHV will keep the team quite small for a long period of time. There are no pressures to grow headcount. Production does not necessarily scale linearly with headcount. Early on, it may be counter-productive. The founders + a few founding engineers will remain a team of <5-10, so they can build & iterate quickly.

Build a product. Test it with customers. Refactor based on data. Rinse. Repeat.

The early team does this until they feel like they have product-market fit. In the case of Sigma Computing, this took 3+ years of experimenting!!!

7) Go fast

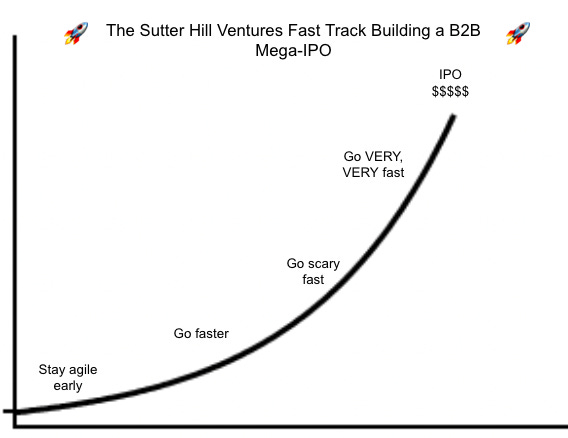

But once they find product-market fit, they scale... really fast.

In Speiser's article on Sigma Computing, he says, "Sigma has product-market fit. Now it’s time to pick up the pace. In 2022 we will go faster. And in 2023 and 2024 we’re going to go scary fast."

In his post prior, Speiser titled the article "Time to go fast." This was announcing Lacework's raise of $1.3B... which will help them, "go very, very fast."

From the outside, it is hard to understand the relative speed of "scary fast" vs. "very, very fast", but basically, the SHV Fast Track looks like Exhibit 7. We will know SHV came across the next Apple when Speiser starts using rocket emojis.

If we use headcount as a proxy, then Lacework has jumped from 128 employees to ~1,040... with an estimated 83 openings still!!!

Structure: Built to build

Up until this point, we have spoken about Sutter Hill's philosophy & process. So why do other firms not copy this?

Well, under the hood, Sutter Hill Ventures is constructed completely differently than most venture firms.

Three principles on structure: 8) Evergreen Fund, 9) Builders in Residence, and 10) Hire Operators.

8) Evergeen fund

Typical venture & private equity firms raise separate funds. Each fund is likely raised with a specific purpose or investment thesis. For example, Andreessen Horowitz is one firm, but CB Insights estimates they have 62 different funds. They have a crypto fund, a consumer fund, etc. The list goes on.

Venture Capitalists will typically develop the thesis & plan, and they will pitch to potential limited partners (LPs). These range from pension funds to high-net-worth individuals. If the potential LP is interested, boom! They invest!

Once the firm determines how much capital (money) they can source, they begin deploying (investing) the fund into companies (aligned with their thesis). Everything varies, but realistically, venture funds will deploy (invest) ALL of the capital (money) commitments for the fund within 2-3 years. This allows investments to mature for 5-7 years, and ideally, by roughly year 10, the firm can start returning gains to their limited partners! (Note: For more info, read this resource)

Why is this at all relevant? Well, the life stage of the fund can impact a firm's ability to invest, and it can lead to wonky incentives. A few limited examples:

Check size: Firms have a set amount of capital they can deploy: the size of the fund. If you raise a set $500M, then you are likely not going to sink $200M+ into one company

Timing: If a firm needs to return capital to limited partners by year 10, then they likely need to get all investments in-market by year 4

Bias to deploy: VCs are paid based on the capital they deploy (management fees) and the gains they produce (carry). Their incentive is to pursue larger funds & deploy 100% of it, potentially independent of the quality of companies available

SHV removes all of this by rejecting the general standard of set funds. SHV only has one fund, and it is evergreen. Meaning... no constraints on when or how they fund companies.

SHV cares about one thing. When they find a good company to invest in, then invest. When they do not, then do not invest.

This gives a lot of firm flexibility to originate companies thoughtfully & scaling capital investments when it is time to "go fast."

9) Hire operators

Probably the most unique part of SHV is "who" they are. Why can they build so much better than other firms?

If you want to build companies, then you probably need to hire people who... wait for it...build! The operators!

This is not necessarily new to venture capital. Plenty of firms hire general partners who previously founded companies, but I think it is fair to say that many firms hire heavily from finance & investing backgrounds, particularly at the lower levels (e.g., analyst, associate).

To benchmark SHV, I scraped the ~75 LinkedIn profiles I could find from the firm.

There are a lot of nuances here, but four primary groups stuck out to me about the structure (reminder: this is outside-in perspective & not validated):

Variety of expertise in core leaders - The managing directors run the show at any firm. In the case of SHV, they have a variety of key backgrounds represented in their leadership

Origination functions - Below the leadership, there is a subset of engineer, design, and ops backgrounds, particularly designated as "in-residence" builders. This team likely handles most of the tactical "origination", supported by the rest of the firm

Centralized operations - The most interesting group of SHV can be found in their operators. Rather than investing backgrounds, SHV hires sales, research, and recruiting backgrounds. This is atypical. My hypothesis is that these core functions help support companies being originated (ex., handle sales motion, tax & finance logistics) and current portfolio companies (ex., centralized recruiting). This is >50% of the entire firm!!!

The investment professionals... or not - Finally, SHV actually has ZERO people that I saw with investing backgrounds. They do not want a former consultant (pains me to say) or investment banker. That is not their game. They want people with hands-on skills that can support their building!

All of these nuances point to a structure designed for building. This is what makes SHV different. Trade in the investment banker for the gritty sales person. Scrap the former consultant making slides, and let's find someone who can go out and recruit.

SHV is uniquely set to build companies because their entire structure, culture, and orientation is based around hiring operators.

10) Builders in Residence

If you look back at SHV companies (ex., Sigma Computing), their founders spent time in tenure as a builder-in-residence within SHV. In my current snapshot, there are seven builders-in-residence, and they more than likely months away from announcing the next wave of SHV companies.

Note: If you want to guess the Stealth companies in Exhibit 1, just go to LinkedIn and look at the builders-in-residence; I can only imagine what they are coming up with!!

What does this actually mean? It means that SHV finds top-tier talent, and they give them a fully-funded position to start building in-house. Supported by a wealth of operational experience like sales, recruiting, etc., the builders-in-residence can spend months tinkering & building their new company.

When the solution is found, the company is created, and the builders-in-residence spin out to found the company!

Now, it is important to note that many other firms have in-residence builders. This is not necessarily unique, but when you consider principles 1-9, it is very easy to see how the SHV builders-in-residence are much more uniquely positioned to succeed.

Conclusion

Speiser's leadership has turned SHV into the silent kingmakers of Silicon Valley, and in my opinion, they are one of the most impressive, yet largely unrecognized, operations in tech. And while their run has been very impressive, they are likely only getting started.

Their success to date has created numerous flywheels. I recommend Kevin Kwok's blog on the Speiser incubation playbook. But for now, just consider the compounding effects of their success.

Three specific flywheels stick out to me:

Talent - Historical success has proven SHV knows what they are doing. This makes it easier to recruit great people. Great people increase chances of success. Which continues to make it easier to recruit

Product testing - 15-20 established SHV companies. Originated companies can test product & get feedback quickly with established companies. This helps them iterate quickly. Faster track to product-market fit increases chances of success

Sales - The ecosystem of employees & potential customers from 15-20 successful Speiser companies is huge. New companies can quickly get in the door. This makes initial sales easier to come by & establish traction. Which leads to higher chances of success

Founding - Second-time founders are known to have an advantage due to experience. What about 10-time founders? Or 20-time? Speiser has done this process MANY times.

There are already some public examples. Snowflake gave trajectory-changing feedback to Sigma Computing. Many of Lacework's early customers were SHV companies. As the SHV ecosystem grows, the flood of talent & customers to originated companies accelerates.

All of this should make us excited for the future. These companies are adding significant value to the corporations we rely on, and overall, I am excited to see what they build next. So if you want to see the next wave of big companies, following SHV origination is a very good place to start.

The narrative I always had in my head was that incubators typically don't work as well as traditional VC spray-and-pray. But maybe that's only true for self-labelled incubators. SHV and Founders Fund are in fact strong incubators, despite not calling themselves that.

There are hundreds of studios it seems these days, but only a few working with top tier talent. Whether at inception or hiring them later, that makes a huge difference.